By Bapon Fakhruddin, Climate Investment Principal, Green Climate Fund

In barely ten days this April, the global water conversation crossed two continents and two very different institutional cultures. On 15 April, the World Bank Group used its Spring Meetings in Washington to launch Water Forward, a new coalition built on a deceptively simple proposition: that water should be treated as foundational climate infrastructure on par with energy and transport. Six days later, delegates gathered in Yeosu, South Korea, for the UNFCCC Climate Week, the first major multilateral milestone on the road to COP31 in Antalya. Different rooms, identical substance. Both confirmed that the climate crisis is, at its core, a water crisis and that the world is not yet financing it like one. The next stop in this sequence is already on the calendar, the UN 2026 Water Conference in Abu Dhabi from 2 to 6 December, where the choreography that began in Washington and matured in Yeosu must harden into commitments.

The industry beneath industries

Water is not a sector; it is the substrate of every sector. UNESCO estimates that 78% of jobs worldwide are moderately to highly water-dependent, a share that rises to 80% in low-income countries and underpins roughly 1.7 billion livelihoods. Yet water is also the most chronically mispriced and underfinanced system we have. In most developing countries, less than 2% of public spending goes to water, while energy can absorb 26% and transport 13% of public spending in the same economies. That asymmetry is not benign; it is corrosive.

The economic evidence is by now unambiguous. Water scarcity, exacerbated by climate change, could cost some regions up to 6% of GDP by 2050. The Bank for International Settlements, drawing on data from 169 countries between 1990 and 2020, finds that a single-standard-deviation rise in water scarcity reduces GDP growth by 0.12 to 0.16% and pushes inflation up by close to three percentage points. The World Resources Institute projects that 31 % of global GDP, roughly 70 trillion dollars, will be exposed to high water stress by 2050, up from 15 trillion in 2010. Water is no longer an environmental concern; it is a binding macroeconomic constraint.

What Yeosu confirmed

Four messages emerged from the water sessions at Climate Week Korea, anchored by the Regional NAP Expo and the parallel Implementation Forum tracks.

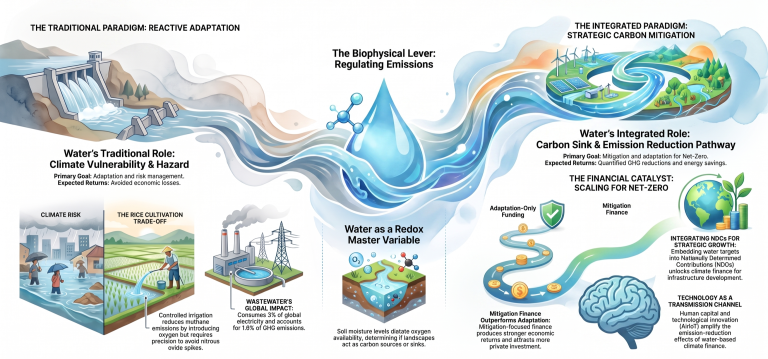

First, the conversation has shifted from naming hazards to diagnosing risk pathways. Delegates moved past the well-rehearsed inventory of floods, droughts, cyclones and saltwater intrusion to a more rigorous question: who is exposed, what vulnerability drivers turn a hazard into harm, and where targeted investment breaks the causal chain. Drought is rarely just a rainfall problem; it is an irrigation access problem. Coastal contamination is rarely due to a single cyclone; it is the compound failure of treatment systems and supply routes following a storm surge. Urban disease outbreaks following extreme rainfall are sanitation deficits revealed under stress. Identifying the driver, whether poverty, weak infrastructure or missing monitoring, is what makes a project bankable.

Second, water security has graduated from a humanitarian framing to a financial one. Muhammad Sharif of the Bank of Maldives captured the mood when he urged the room to move from promises to portfolios, financing desalination, solarisation and water security systems as existential investments for small island states rather than as concessional charity.

Third, water is being formally embedded inside National Adaptation Plans (NAPs) rather than appended to them. Egypt, through the SCALA project, is defining sector-specific targets across the water-agriculture nexus to support early warning systems. Papua New Guinea has placed water, sanitation and hygiene among the nine priority areas of its NAP. Türkiye’s national strategy lists water resources management as one of 11 key sectors, tracked through an online monitoring system. These are the connective tissues that allow ministries of finance, line ministries, and external financiers to transact on the same data.

Fourth, the implementation gap is now the defining problem. Over 90 % of countries’ NDCs and NAPs already prioritise water-related adaptation, so the demand signal is unmistakable. Yet global adaptation finance reached only 28 to 29 billion dollars in 2023, against a need of more than 300 billion dollars per year by 2030. Within that constrained pool, water receives roughly 40 %, the largest single share, and still nowhere near sufficient. Estimates from the World Bank and the United Nations put annual needs at 114 to 150 billion dollars through 2030 just to meet water supply, sanitation and resource management targets. The World Economic Forum, in partnership with the University of Cambridge, estimates a cumulative water infrastructure shortfall of 6.5 trillion euros by 2040, or roughly 435 billion euros per year, and finds that every euro invested returns 1.30 euros in gross value added, with the potential to create 206 million jobs.

The Green Climate Fund and the 2030 horizon

Climate Week’s location in Korea was not incidental. The Asia Pacific region holds the most concentrated portfolio of water and climate risk on Earth, from receding Himalayan glaciers to intensifying and erratic monsoons, to coastal megacities confronting flooding and saltwater intrusion at the same time. The Republic of Korea’s decision to co-stage the UNFCCC Climate Week with its Green Transformation International Week, and its interest in eventually hosting COP33 in 2028, signal an ambition to lead on the implementation agenda rather than merely host it.

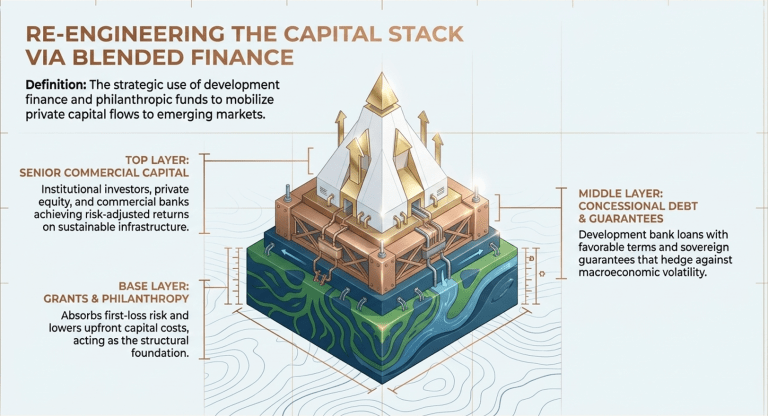

That logic is now embedded in our 2030 ambition. GCF has committed to reaching 384 million people and restoring 82 million hectares by 2030, with water security, flood protection and ecosystem-based adaptation among the largest contributors to those targets. To date, we have already mobilised over 4 billion dollars across more than 80 climate resilient water security projects in over 100 countries, expected to benefit close to 40 million people through improved water access, flood protection and sanitation. A significant share of the global water financing now flowing through climate finance is catalysed by GCF concessional capital, blended financing where early-stage public risk capital opens space for commercial banks, insurers, sovereign investors and project sponsors to enter at scale.

At Yeosu, GCF’s role was deliberately operational, leading dialogues on readiness, gender responsive climate finance and country platforms, while highlighting the project pipelines and risk-sharing instruments that make water investments viable for the private sector. Two weeks earlier, the Climate Solutions Week in Vienna had convened a high-levelTime is the variable we keep underestimating. The UN SDG 6 Synthesis Report for 2026 warns that, at the current rate, the world will not achieve sustainable water management until at least 2049, a full twenty three years from now. That is not a delay, it is a generational miss, and every year of underinvestment compounds the cost of catching up. Each missed flood defence, each unbuilt desalination plant, each utility left without a credible balance sheet, becomes tomorrow’s emergency appeal.

Abu Dhabi this December and COP31 in Antalya next year are the two moments where that trajectory can still be bent. They are not ceremonial waypoints, they are the venues where finance ministers, regulators, development banks, climate funds and private investors will have to decide whether water moves from the margins of the climate agenda to its centre. The implementation era will be defined by who builds the architecture to turn ambition into capital flows, and water, long treated as a humanitarian afterthought, will be where that architecture is judged first.

Washington opened the conversation. Yeosu road tested the engineering. Abu Dhabi must now turn the ignition. The countries and institutions that move quickly, by prioritising water in their budgets, in their climate strategies and in their capital markets, will be best positioned for a century already being shaped by water. Those that continue to undervalue this most essential of resources will pay in GDP, in jobs, in food security and in human dignity.

Water is part of everything. It is time we invested like it, before the window closes on us. water roundtable of MDBs, DFIs, philanthropies and governments to align commitments behind a shared water mission. Vienna, Washington and Yeosu were sequential rehearsals for a single delivery system, and Abu Dhabi in December is where that system has to perform.

What has to change

Five priorities now define the agenda. None are new, all are urgent.

Price water honestly. The Global Commission on the Economics of Water concluded that the hydrological cycle remains severely underpriced and under protected. Phasing out perverse subsidies and reflecting true scarcity in tariffs is the precondition for any private investment thesis.

Raise the water share of public budgets. A sector that receives less than 2 percent of public spending will not attract private capital, no matter how well designed the climate funds behind it.

Industrialise the project pipeline. NAPs and NDCs must be translated into bankable, measurable, sequenced investment plans that ministries of finance and external investors can transact on without bespoke negotiation each time.

Build creditworthy institutions. Utilities, river basin authorities and subnational providers must be reformed to a standard where institutional investors can transact with them directly. This is governance work, and it cannot be outsourced to a financing instrument.

Use innovative concessional finance to crowd in, not crowd out, private capital. Guarantees, first loss tranches, foreign exchange hedging facilities, results based payments and outcome bonds should be deployed where they unlock private sector engagement at scale, not where they substitute for it. This is the space in which GCF and its partners are positioned to lead.

The window is closing

Time is the variable we keep underestimating. The UN SDG 6 Synthesis Report for 2026 warns that, at the current rate, the world will not achieve sustainable water management until at least 2049, a full twenty three years from now. That is not a delay, it is a generational miss, and every year of underinvestment compounds the cost of catching up. Each missed flood defence, each unbuilt desalination plant, each utility left without a credible balance sheet, becomes tomorrow’s emergency appeal.

Abu Dhabi this December and COP31 in Antalya next year are the two moments where that trajectory can still be bent. They are not ceremonial waypoints, they are the venues where finance ministers, regulators, development banks, climate funds and private investors will have to decide whether water moves from the margins of the climate agenda to its centre. The implementation era will be defined by who builds the architecture to turn ambition into capital flows, and water, long treated as a humanitarian afterthought, will be where that architecture is judged first.

We opened the conversation starting the year. Yeosu road tested the engineering. Abu Dhabi must now turn the ignition. The countries and institutions that move quickly, by prioritizing water in their budgets, in their climate strategies and in their capital markets, will be best positioned for a century already being shaped by water. Those that continue to undervalue this most essential of resources will pay in GDP, in jobs, in food security and in human dignity.

Water is part of everything. It is time we invested like it, before the window closes on us.