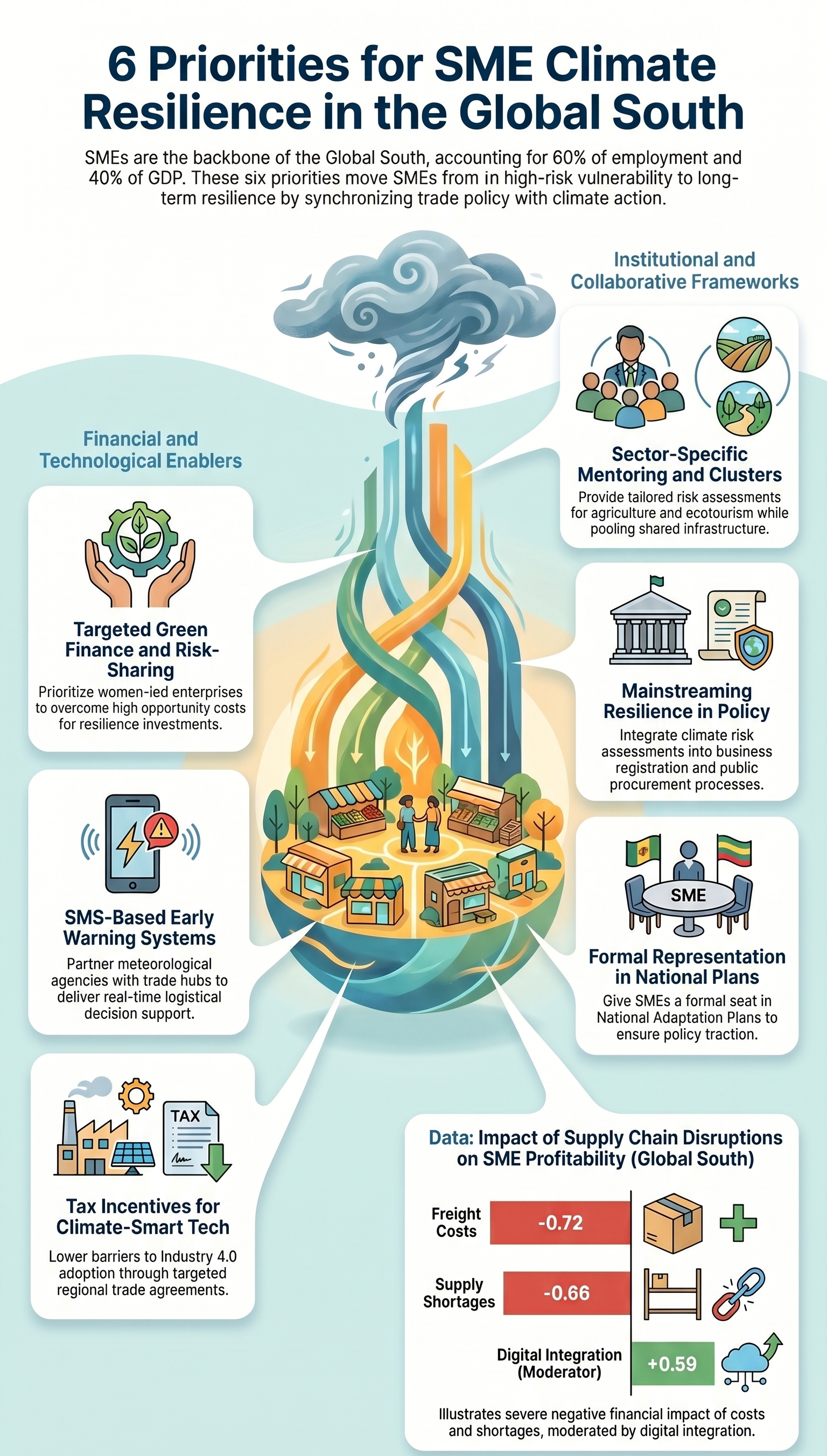

When a flash flood washes out a feeder road in the Mekong Delta, or a drought withers a smallholder’s maize in the Sahel, headlines fixate on hectares lost and tonnes of grain forgone. The quieter casualty is the small business owner. The woman aggregating produce, the cooperative shipping coffee, and the workshop welding irrigation pumps. Her ledger absorbs the shock long before any compensation arrives. Small and medium-sized enterprises account for roughly 60 per cent of employment and 40 per cent of GDP across the Global South. They are also the front line of climate impact. If we are serious about inclusive growth in a warming world, the resilience of the global economy must be measured by the resilience of its smallest firms.

At the Green Climate Fund, we have spent the last several years testing what works to keep these firms standing. The pattern that emerges, captured in our six priority framework, is not a menu of isolated interventions. It is a single integrated proposition. De-risk the market, and the market will finance the transition.

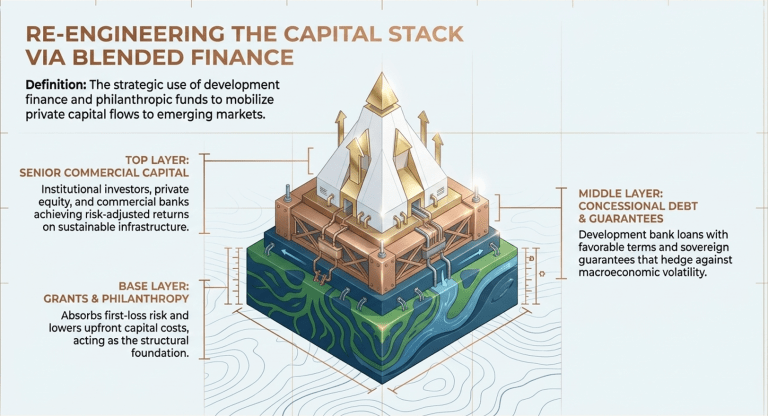

First, finance must meet SMEs where they are. Commercial lenders rarely write tickets for a maize cooperative or a women-led agro-processor. The upfront costs are high, the collateral thin, and the climate risk poorly priced. GCF’s response has been blended finance at scale. In East Africa, our ARCAFIM facility channels concessional credit through local banks to fund SME adaptation, crowding in private capital. In our regenerative agriculture programme across several African countries, GCF takes junior positions and provides technical assistance, catalysing roughly 300 million dollars in co-investment and reaching over 1.1 million livelihoods, the majority of which are women. Partial credit guarantees and first-loss tranches do the rest, lowering collateral requirements and drawing lenders into segments they once avoided.

Second, information is infrastructure. A weather alert on a farmer’s phone the night before a storm is worth more than a subsidy paid the month after. GCF’s FP270 project in Cambodia builds integrated agrometeorological services so smallholders receive village-level forecasts. Extreme weather becomes a manageable variable rather than a catastrophic risk. The same logic applies to an exporter calibrating shipping around a cyclone forecast, or a cold chain operator hedging against a heatwave. SMS based early warning systems and digital advisory platforms are not gadgets. They are the connective tissue between climate science and a balance sheet.

Third, technology transfer must be deliberate. Solar irrigation, drought-tolerant seed, and supply chain traceability tools are the inputs that let small producers meet rising sustainability standards in export markets. Without targeted financing and tax incentives for climate-smart adoption, the productivity gap widens, and the trade gap with it.

Fourth, policy must reward resilience, not penalise it. Through Readiness grants, GCF works with governments to embed climate criteria into procurement, export standards, and tax codes. When a procurement rule rewards suppliers who have adapted, resilience stops being a cost center and becomes a market advantage. Policy without a private sector voice is policy without traction. Synchronising trade policy with climate action is not a soft development priority. It is the only credible path to inclusive growth.

Fifth, capacity must be built in clusters. Sector accelerators, mentoring networks, and supplier clusters give cooperatives, ecotourism operators, and clean energy startups the scale and standards needed to enter global value chains. A single farmer cannot certify a coffee shipment to European buyers. A two-thousand-member cooperative can.

Sixth, institutions must hold the system together. The most fragile element of any resilience strategy is the assumption that someone will keep coordinating after the project closes. GCF investments deliberately strengthen national agencies, water user associations, and SME chambers, and link them to global platforms such as the ITC Trade for Sustainable Development initiative and the Alliance for Financial Inclusion. Formal representation of SMEs in National Adaptation Plans is not a procedural nicety. It is how a maize cooperative in Zambia or a textile workshop in Ethiopia ends up in the same conversation as central banks and trade ministries.

The lessons travel. What is working in CAISAR, namely resilient infrastructure, hyperlocal climate information, and multi-level institutional support, is directly transferable to African contexts where rain-fed agriculture and informal logistics carry similar exposure. Adaptation programmes from the Sahel to East Africa are already bundling advisories with microloans, blending finance for irrigation upgrades, and training cooperatives in climate-smart agriculture.

The math is unforgiving but clarifying. If freight shocks and supply shortages can erase two-thirds of SME profitability, and digital integration can recover more than half of that loss, the policy choice is obvious. We can keep treating SME resilience as a charity line item, or recognise it as the load-bearing wall of the global trading system.

Catalyzing climate resilient SMEs is not an act of generosity. It is the most pragmatic investment we can make in the stability of trade, the credibility of climate finance, and the dignity of work in the regions that will define this century.